Recent POST

When you pick up your prescription at the pharmacy, you might not think about why your generic blood pressure pill costs $10 while the brand-name version is $75. But behind that price difference is a complex system designed by your employer’s health plan - one that pushes you toward cheaper drugs, often without you even realizing it. This isn’t about cutting corners. It’s about structure. And if you don’t understand how it works, you could be paying way more than you need to.

How Your Employer’s Drug Plan Is Built

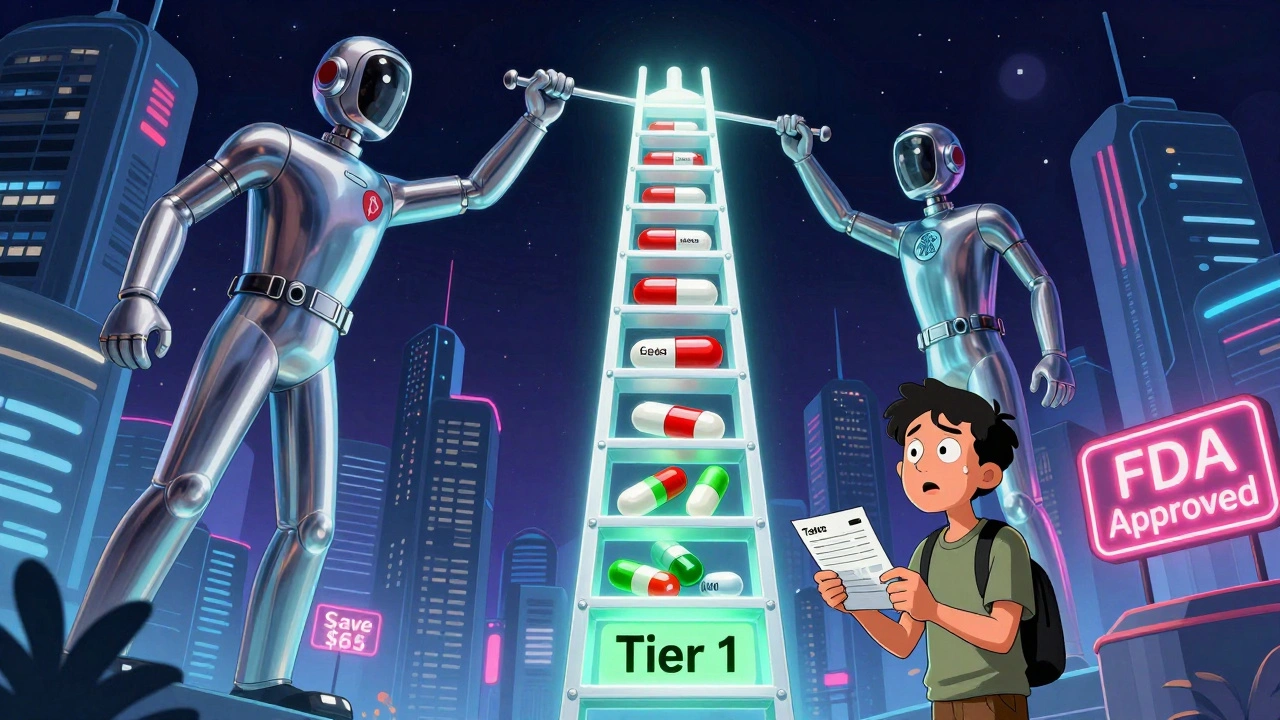

Most employer health plans don’t just cover all prescriptions the same way. Instead, they use something called a formulary - a list of approved medications grouped into tiers based on cost. Think of it like a pricing ladder. The lower the tier, the less you pay out of pocket. Tier 1 is almost always reserved for generic drugs. These are chemically identical to brand-name versions but cost 80-85% less. The FDA confirms they’re just as safe and effective. Tier 2 usually includes preferred brand-name drugs - ones your plan has negotiated better deals on. Tier 3 is for non-preferred brand-name drugs, which cost more because your plan didn’t get a good deal on them. And Tier 4? That’s where specialty drugs live - things like biologics for rheumatoid arthritis or cancer treatments. Those can cost hundreds or even thousands per month. Here’s what that looks like in real dollars, based on typical employer plans in 2025:- Tier 1 (generic): $10 copay

- Tier 2 (preferred brand): $40 copay

- Tier 3 (non-preferred brand): $75 copay

- Tier 4 (specialty): 25-33% coinsurance (you pay a percentage of the total cost)

That $65 difference between a generic and a non-preferred brand isn’t just a suggestion - it’s a financial nudge. And it works. Over 99% of large employer plans include some form of prescription coverage, and nearly all of them use this tiered model.

Why Generics Are Pushed So Hard

You might wonder why your employer cares so much about generics. The answer is simple: money. Every week, generic drugs save the U.S. healthcare system $3 billion. That’s over $150 billion a year. For employers, that’s not just a savings line item - it’s a major factor in keeping health insurance premiums from skyrocketing. But here’s the catch: the savings don’t always reach you. The middlemen - Pharmacy Benefit Managers (PBMs) like OptumRx, CVS Caremark, and Express Scripts - negotiate rebates with drug manufacturers. These rebates can be huge. KPMG found the average “gross-to-net” spread is 55%. That means if a drug’s list price is $100, the PBM might only pay $45 after rebates. But you still pay the full $75 copay for the brand-name version, even though the PBM got a deep discount. That’s the disconnect. The system saves billions, but you don’t always see it on your receipt. Your employer benefits from lower overall costs, and the PBM pockets the rebate. You? You’re stuck paying the higher price unless you choose the generic.What Happens When a Brand Turns Generic

When a brand-name drug loses its patent, a generic version hits the market. That’s good news - for everyone, right? Not always. Your PBM will automatically move the generic to Tier 1. The brand-name version? It gets kicked to Tier 4. Suddenly, the drug you’ve been taking for years now costs $75 instead of $10. And if your doctor doesn’t switch your prescription, you’re stuck paying the difference. This isn’t rare. In January 2024, each of the three biggest PBMs removed over 600 drugs from their formularies. Many of those were older brand-name drugs that had just gone generic. The message was clear: if you want this drug, take the generic - or pay a lot more. And it’s not just about cost. PBMs use formulary exclusions as bargaining chips. If a drugmaker won’t give a big enough rebate, the PBM simply drops the drug. No warning. No grace period. One day it’s covered. The next, it’s not.

How to Find Out What’s Covered

You can’t rely on memory or your doctor’s word alone. Formularies change all the time. A drug covered this month might be excluded next month. Here’s how to stay in control:- Visit your insurer’s website. Look for the “Drug List” or “Formulary” section. This is the official list of covered drugs.

- Check your Summary of Benefits and Coverage (SBC). It’s a short document your employer must give you every year. It breaks down your copays by tier.

- Call your insurer. Ask: “Is my medication on the formulary? What tier is it on? Is there a generic alternative?”

- Ask your pharmacist. They see formulary changes daily and can tell you if your prescription will be denied or cost more than expected.

Don’t wait until you’re at the counter. Do this before your prescription runs out. If your drug gets removed, you’ll need time to work with your doctor on an alternative - or request a medical exception.

What to Do If Your Drug Gets Dropped

If your medication disappears from the formulary, you’re not out of options. First, ask your doctor if a generic or preferred brand is available. Most of the time, there is. If not, you can file a “prior authorization” or “medical necessity exception.” This means your doctor writes a letter explaining why you need the specific drug - maybe because you had side effects with generics, or the generic doesn’t work as well for you. Your employer’s HR department can help you with this process. Many large plans have care managers who specialize in helping employees navigate these roadblocks. HealthOptions.org, for example, offers programs where care managers find ways to get you the medicine you need at a price you can afford. Don’t assume you’re stuck paying full price. Formulary exclusions are negotiable - if you act fast.

How Employers Are Changing the Game

More employers are moving toward Consumer Driven Health Plans (CDHPs). These plans pair high-deductible insurance with health savings accounts (HSAs). The idea? Give employees more control - and more incentive - to make smart choices. In CDHPs, the cost difference between generics and brands is even starker. You’re paying more out of pocket anyway, so choosing a $10 generic over a $75 brand makes financial sense. Employers are also starting to use payroll stuffers, emails, and even social media to educate employees about generics. Why? Because many people still think generics are “weaker” or “lower quality.” They’re not. But they won’t switch unless they understand why. Some employers are even partnering with pharmacies to offer automatic discounts on generics. Programs like HealthOptions.org’s “Price Assure Program” lower your cost at the register without you having to ask.What This Means for You

Your employer’s health plan isn’t trying to trick you. It’s designed to save money - and it’s working. But the system is complex, opaque, and constantly shifting. Your job? Stay informed. Know your formulary. Ask questions. Don’t assume your prescription will stay covered. If you’re on a chronic medication - for diabetes, asthma, high blood pressure, or heart disease - make sure you’re on the lowest tier possible. If you’re not, ask why. And if you’re still unsure? Talk to your pharmacist. They’re on the front lines. They know what’s covered, what’s not, and what alternatives exist. They’ve seen this play out thousands of times. The bottom line: generics aren’t just cheaper. They’re just as good. And in most cases, they’re your best option - if you know how to use the system to your advantage.What’s Next for Employer Drug Coverage

The trend isn’t slowing down. PBMs are getting more aggressive with formulary exclusions. Drug prices keep rising. Employers are under pressure to keep premiums low. That means more drugs will be moved off formularies. More generics will be pushed. More rebates will be negotiated behind the scenes. The big question: will the savings ever reach you directly? Right now, the answer is mostly no. But as public pressure grows and lawmakers start looking at PBM rebates, that could change. For now, your best defense is knowledge. Know your plan. Know your drugs. Know your options. Because when it comes to prescription coverage, the system works best for those who understand it.Are generic drugs really as good as brand-name drugs?

Yes. The FDA requires generic drugs to have the same active ingredients, strength, dosage form, and route of administration as the brand-name version. They must also meet the same strict standards for quality, safety, and effectiveness. The only differences are in inactive ingredients (like fillers or dyes) and packaging. Generics are not “weaker” or “inferior.” They’re just cheaper because they don’t carry the cost of marketing or clinical trials.

Why does my generic cost more this month?

Your plan’s formulary may have changed. Even if the drug is still generic, your insurer could have moved it to a higher tier, switched pharmacies, or changed their rebate agreements. PBMs update formularies frequently - sometimes without notice. Always check your drug list before refilling a prescription.

Can my employer force me to switch to a generic?

No, they can’t force you. But they can make it financially difficult. If your plan moves the brand-name version to Tier 4 and the generic to Tier 1, you’ll pay $65 more per prescription. Most people choose the generic because of the cost difference - not because they’re forced to.

What if I need a drug that’s not on the formulary?

You can request a medical exception through your insurer. Your doctor must submit documentation explaining why the drug is medically necessary - for example, if you’ve tried all alternatives and had adverse reactions. If approved, your plan will cover it. If denied, you can appeal. Don’t assume it’s impossible - many exceptions are granted.

Do all employer plans have the same formulary?

No. Formularies vary widely depending on your insurer and employer plan. Anthem, for example, offers six different drug lists for different employer plans in Ohio. Even within the same company, two employees might have completely different formularies based on which plan they chose. Always check your specific plan’s list - don’t assume yours matches someone else’s.

How often do formularies change?

Formularies can change at any time. PBMs update them monthly or even weekly, especially when new generics hit the market or when rebate deals expire. There’s no legal requirement for advance notice. That’s why checking your drug list before each refill is critical.

Can I switch to a different plan to get better coverage?

Only during open enrollment or if you have a qualifying life event - like a birth, marriage, or job change. Outside of those windows, you’re stuck with your current plan. That’s why it’s so important to understand your plan’s formulary before you enroll.

aditya dixit

It's wild how much of our healthcare is run like a corporate spreadsheet. Generics aren't just cheaper-they're scientifically identical. The real issue isn't the drugs, it's the middlemen who profit from the confusion. If we cut out the PBM rebate black box, we could lower costs for everyone without sacrificing quality. Simple math, but nobody talks about it.

Rupa DasGupta

lol so now my blood pressure med is a "financial nudge"? 🤡 I swear if I see one more "choose generic" email from HR I'm gonna start taking my pills on Tuesdays only. Also my last generic tasted like burnt plastic. Not a metaphor. Actual burnt plastic. 🤢

Marvin Gordon

Stop treating patients like accountants. The system isn’t broken-it’s designed to confuse you into compliance. If you’re paying $75 for a brand-name pill while the generic is $10, that’s not a nudge, that’s a penalty. And yeah, generics work. I’ve been on them for 12 years. No side effects. No drop in efficacy. Just lower bills. Wake up, people.

ashlie perry

Did you know PBMs are owned by big pharma and insurance companies? They’re not even real companies-just shells. They create fake rebates so you pay more, then they say it’s for your own good. This is how they control us. They don’t want you to know generics are the same. They want you scared. Watch what happens when they ban all generics next

William Chin

It is imperative to underscore that the structural architecture of pharmaceutical formularies is not merely a fiscal mechanism, but a regulatory instrument designed to optimize therapeutic outcomes through cost-containment protocols. One must not conflate economic efficiency with clinical inferiority, as the FDA’s bioequivalence standards are unequivocally rigorous and non-negotiable.

Ada Maklagina

My pharmacist told me the same pill I’ve been on for 5 years just got moved to tier 4. I asked why. She shrugged and said "rebates". I asked if I could get the generic. She said "yes, but your doctor has to write a new script". So now I have to call my doctor, wait 3 days, then go back to the pharmacy. All for a pill that’s chemically the same. This isn’t healthcare. It’s bureaucracy with a smiley face.

Chris Brown

It is morally indefensible that individuals are penalized financially for not conforming to corporate formulary dictates. The fact that a life-sustaining medication is rendered inaccessible through tiered pricing constitutes a form of economic coercion. One cannot claim to value health while simultaneously designing systems that make adherence contingent upon economic compliance.

Jennifer Patrician

They’re lying. PBMs are in cahoots with drug companies. The generics are actually made in the same factories as the brand names. Same exact pills. Same exact workers. Same exact packaging. The only difference? The label. They charge you extra so they can pocket the rebate. And your HR department? They’re in on it. They get kickbacks from the PBM for pushing generics. That’s why they send you those emails. That’s why they call it "education". It’s manipulation.

Ali Bradshaw

Just wanted to say-this is the kind of post that should be mandatory reading for every employee during onboarding. I wish someone had explained this to me when I first got my job. I paid $80 for a brand-name statin for two years because I thought generics were "second-rate". Turned out my body reacted worse to the brand. Switched to generic. Same effect. $10 copay. No more headaches. No more guilt. Just… relief. Don’t overthink it. Ask your pharmacist. They’ve seen it all.

Write a comment